Fourth Quarter 2017

Questions and Answers

January 31, 2018

Cautionary Note Regarding Forward-Looking Statements

This document contains information that may constitute “forward-looking statements” within the meaning of Section 27 of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We intend the forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in those sections. Generally, we have identified such forward-looking statements by using the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “target,” “forecast,” “aim,” “should,” “will” and similar expressions or by using future dates in connection with any discussion of, among other things, operating performance, trends, events or developments that we expect or anticipate will occur in the future, statements relating to volume

growth, share of sales and earnings per share growth, and statements expressing general views about future operating results. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. Forward-looking statements are not historical facts, but instead represent only the Company’s beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside of the Company’s control. It is possible that the Company’s actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in these forward-looking statements. Management believes that these forward-looking statements are reasonable as of the time made. However, caution should be taken not to place

undue reliance on any such forward-looking statements because such statements speak only as of the date when made. Our Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our Company's historical experience and our present expectations or projections. These risks and uncertainties include, but are not limited to the risks and uncertainties described in “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2016, and those described from time to time in our future reports filed with the Securities and Exchange Commission. References to "we," "us," "our," the "Company," and "U. S. Steel," refer to United States Steel Corporation and its consolidated subsidiaries.

| |

1. | How will the Tax Cuts and Job Acts of 2017, that was signed into law by the President in December, impact your results? |

Enactment of tax reform resulted in an $81 million ($0.46/diluted share) benefit to U. S. Steel in the fourth quarter of 2017. This was driven by the remeasurement of our deferred tax liabilities at the lower rate, and the release of the valuation allowance on deferred tax assets associated with alternative minimum tax (AMT) credits. The new law has eliminated AMT beginning with the 2018 tax year, and has provided a means for companies to receive refunds for existing AMT credits over the next 5 years. We expect to receive approximately $70 million in refunds in 2019 – 2022.

There was no earnings impact associated with remeasuring our deferred tax assets because of the full valuation allowance offsetting the deferred tax assets.

We expect that our future effective tax rate will be less than the statutory rate of 21% because of the depletion deduction available to use from our mining operations.

Given our current net operating loss (NOL) position, we do not see any immediate impact/benefit to us because of the full expensing provisions.

| |

2. | What is the status of the Section 232 investigation on steel imports? |

On April 19, 2017, the Secretary of Commerce initiated an investigation under Section 232 of the Trade Expansion Act of 1962 to determine the effects of steel imports on U.S. national security. On May 24, 2017, we testified at the U.S. Department of Commerce (DOC) public hearing. We continue to advocate for broad Presidential action under Section 232. Our Nation cannot afford to allow the continued rise of foreign imports that undermine America’s capacity to produce the steel necessary for our country’s national and economic security.

On January 11, 2018, the Secretary of Commerce submitted DOC’s findings from the investigation to the President. Under the statute, the President has until April 11, 2018 to decide what action, if any, to take to adjust imports found by DOC that harm national security. Within 15 days of the President’s decision, the action must be implemented. Within 30 days of the decision, a summary of DOC’s findings and a statement on the President’s reasoning to take, or not take, action must be submitted to Congress and published in the Federal Register.

| |

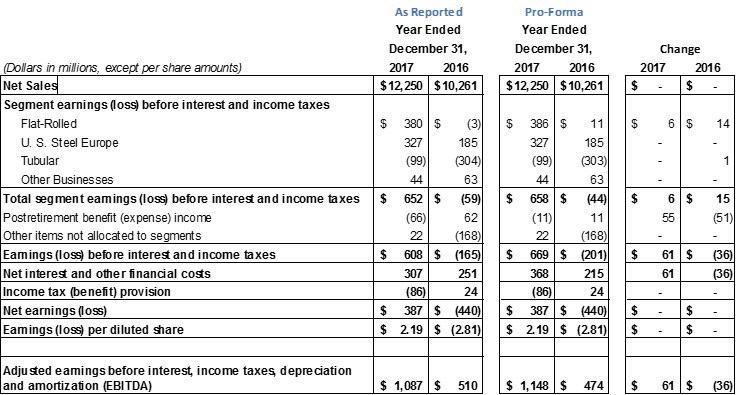

3. | Why is your reporting of postretirement benefit (expense) income changing in 2018, and how will the change impact your financial results? |

Effective January 1, 2018, U.S. Generally Accepted Accounting Principles (U.S. GAAP) has changed how an employer who offers defined benefit and postretirement benefit plans reports the service cost component of the net periodic benefit cost and the other components of net periodic benefit cost (ASU 2017-07). Service cost will be reported in the same line item or items as other compensation cost arising from services rendered by employees during the period, primarily cost of sales and selling, general and administrative expense. The other components of net periodic benefit costs will be presented on a retrospective basis in the income statement separately from the service cost component and will be reported in net interest and other financial costs.

The adoption of this new accounting standard will not have an impact on our net earnings (loss) but it will result in a reclassification from a line on the income statement within earnings (loss) before interest and income taxes to a line on the income statement below earnings (loss) before interest and income taxes.

The table below shows the pro-forma impact of reporting under ASU 2017-07 on our 2016 and 2017 results.

| |

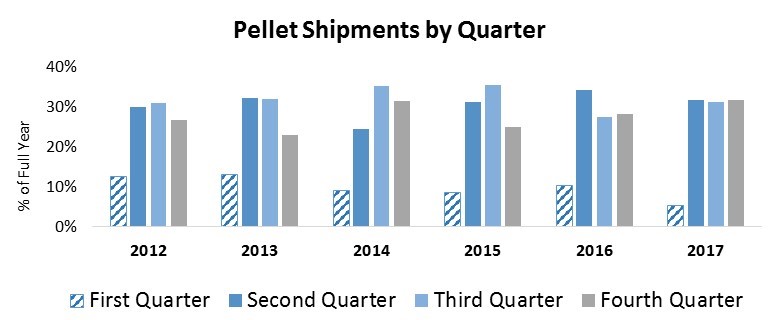

4. | How does the seasonality of iron ore shipments impact your financial results? |

Our mining operations are unable to ship pellets to our blast furnaces in the U.S. and to our third-party customers for much of 1Q because the Soo Locks, which connect Lake Superior with the lower Great Lakes, are typically closed from mid-January to late March. Our mining operations still produce pellets in those months, but at a lower volume. This scenario negatively impacts our financial results due to the operating inefficiencies that result from running at lower production volumes with increased spending due to planned maintenance resulting in a higher cost per ton.

The graphic below illustrates the seasonality of pellet shipments.

| |

5. | What is your exposure to changes in global metallurgical coal costs? |

We expect our delivered coal cost for our U.S. operations in 2018 to be comparable to our 2017 coal costs.

Our annual coal requirements have decreased as we permanently shut down cokemaking capacity concurrent with the permanent shutdown of steelmaking capacity in 2014. Our current domestic cokemaking operations, plus the Suncoke Gateway operations, running at full capacity would consume approximately 6.5 to 7.0 million tons of coal annually, which would support approximately 16 million tons of raw steelmaking capacity.

We purchase coal for our European operations under arrangements that typically have quarterly pricing resets. Our European cokemaking operations running at full capacity would consume approximately 2 million tons of coal annually, which would support approximately 4.5 million tons of raw steelmaking capacity.